When Ethiopia loosened its grip on the foreign-exchange market, policymakers framed the move as a technical correction — a necessary alignment of the birr with economic reality. In practice, deregulation has proved to be something larger: a structural reset that is reshaping inflation dynamics, trade flows and balance-sheet risk across the economy.

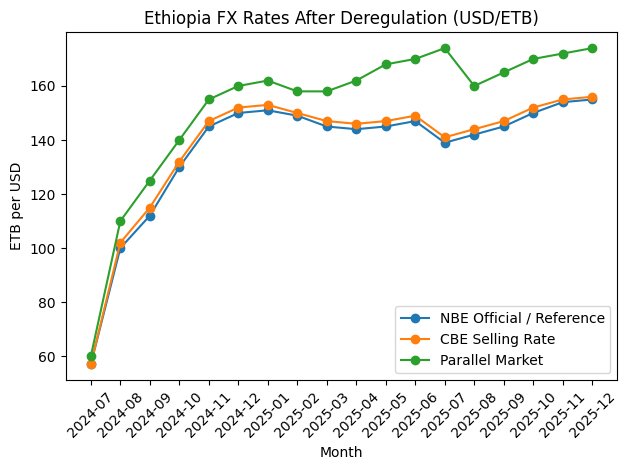

The FX data since deregulation — drawn from National Bank of Ethiopia reference rates, Commercial Bank of Ethiopia selling prices and parallel-market indicators reported by Capital and Addis Fortune — show a clear break with the past. The birr has not weakened smoothly. It has adjusted in steps, punctuated by policy events, liquidity squeezes and shifts in expectations. That pattern matters, because it determines how costs, prices and risks propagate through the economy.

A regime change in the exchange rate

The FX line graph tells the story more clearly than any policy communiqué. In mid-2024, the official reference rate jumped sharply lower against the dollar, followed by a rapid repricing by commercial banks. The parallel market moved in tandem, preserving a premium that narrowed but never disappeared.

This was not liberalisation in the textbook sense of a continuous, market-clearing price discovery process. It was a controlled reset. The state stepped back from defending an artificial level, but scarcity — of reserves, of inflows, of confidence — continued to define the market.

Since then, the birr has drifted weaker in uneven increments. Periods of apparent stability have tended to reflect temporary liquidity management rather than a durable improvement in fundamentals. By late 2025, the upward slope of all three FX curves suggests that expectations of further depreciation remain embedded.

Inflation: faster pass-through, less insulation

The most immediate consequence has been a change in how inflation behaves. Before deregulation, exchange-rate pressure was often absorbed through delays, rationing and implicit subsidies. Price pass-through existed, but it was slow and uneven.

Post-deregulation, the lag has shortened dramatically. Import-dependent sectors now reprice almost immediately following FX adjustments. Automotive spare parts, construction materials, pharmaceuticals and industrial inputs are typically priced using either the parallel rate or an implicit blend of official and informal rates. Even when the official rate pauses, inflation pressure persists as long as the parallel market remains elevated.

Transport and logistics amplify the effect. Fuel pricing, vehicle parts and freight costs transmit FX shocks across food markets and manufactured goods. The result is not only higher inflation, but more volatile inflation — harder for households to anticipate and more difficult for policymakers to anchor.

Importers under pressure, exporters with caveats

For importers, deregulation has clarified prices but raised risk. Letters of credit have become more expensive not just because the birr is weaker, but because banks now price volatility itself. Shorter quotation windows and wider spreads reflect balance-sheet caution rather than opportunism.

Many importers report that access to FX at quoted rates is as important as the rate level itself. In this sense, deregulation has shifted uncertainty from administrative approval to market availability.

Exporters, in theory, should be the beneficiaries. A weaker birr boosts birr-denominated revenues and improves price competitiveness. In practice, the gains are uneven. Input costs — fuel, packaging, machinery and transport — rise in tandem with depreciation. For exporters with long production cycles, the step-wise nature of FX adjustment complicates planning and hedging.

Coffee exporters and manufacturers may see improved margins in accounting terms, but only if FX access is timely and domestic cost inflation does not outpace currency gains. Deregulation has delivered clarity, not comfort.

Banking and balance-sheet effects

One of the least visible but most consequential impacts has been on corporate balance sheets. Firms with foreign-currency liabilities have seen their obligations revalued sharply at each FX adjustment point. For companies with thin capital buffers, this has eroded equity and constrained borrowing capacity.

Banks, meanwhile, sit at the center of the transmission mechanism. The Commercial Bank of Ethiopia’s selling rate closely tracks the NBE reference, but consistently above it — a buffer reflecting liquidity risk, regulatory costs and uncertainty. That spread is not merely a technical margin; it is the price of operating in a market where FX is scarce and expectations remain unsettled.

A new operating reality

Taken together, the FX data point to a new economic regime. Ethiopia has moved away from a static, policy-determined exchange rate towards a managed but volatile system in which expectations play a central role. The parallel market has lost some of its distortive power, but it continues to set the ceiling for pricing behaviour across much of the economy.

For policymakers, the challenge has shifted. The question is no longer how to defend a level, but how to manage expectations and smooth adjustment. Clear communication, predictable liquidity provision and credible reserve management now matter as much as formal policy settings.

For businesses, adaptation is unavoidable. Hedging instruments remain limited, but operational hedges — faster inventory turnover, diversified sourcing, FX-indexed contracts — are becoming standard practice. Investment decisions are shorter-dated, and risk premiums are rising.

The FX charts do not suggest imminent stability. They do, however, make one thing clear: Ethiopia’s deregulation has changed the rules of the game. Inflation, trade and financial risk are now linked more directly to the exchange rate than at any point in recent history — and the economy is still learning how to live with that reality.