By any recent standard, Ethiopia’s fuel price trajectory has been steep. Since the start of 2023, official pump prices for diesel, gasoline and kerosene have risen in a series of measured but persistent steps, reshaping cost structures across transport, construction, agriculture and trade.

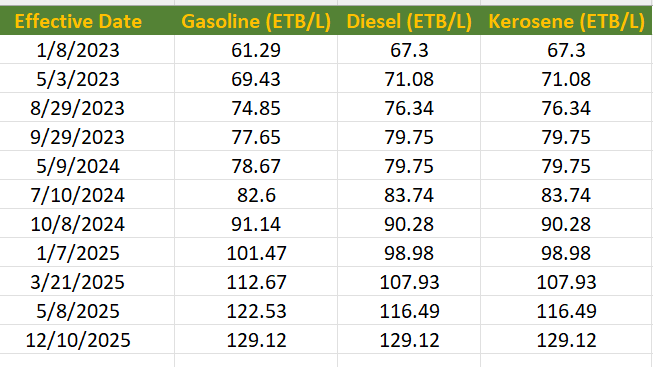

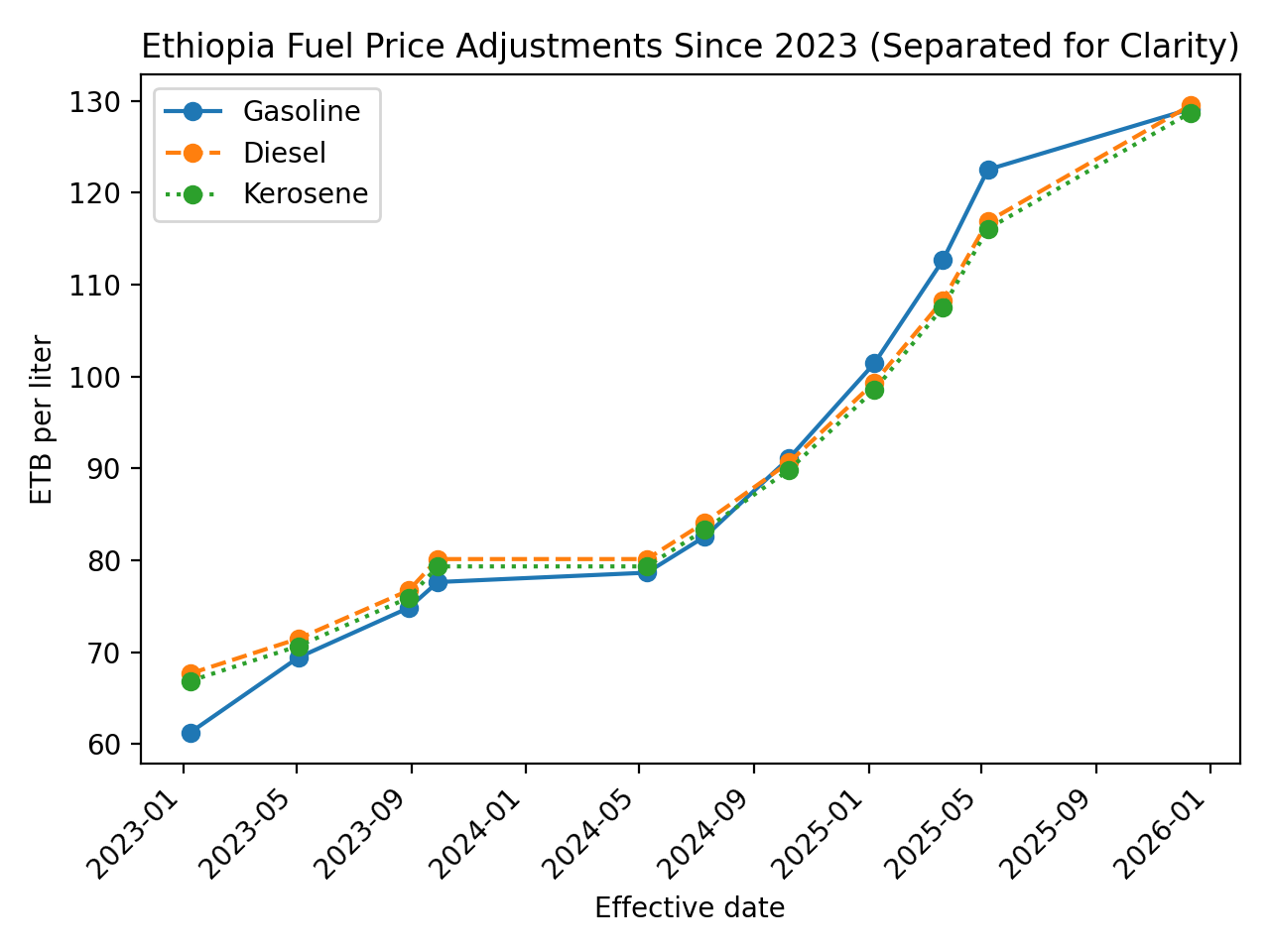

In January 2023, gasoline sold at 61 birr per litre, while diesel and kerosene stood at 67 birr. By December 2025, all three fuels had converged at 129 birr per litre, representing an increase of more than 100 per cent for gasoline and almost 92 per cent for diesel and kerosene in less than three years. Few other policy-adjusted prices have moved as decisively, or with such economy-wide consequences.

A gradual climb — until it wasn’t

For much of 2023 and early 2024, fuel price adjustments followed a relatively predictable rhythm. Increases were frequent but incremental: gasoline rose to around 75 birr per litre by August 2023, then to 78 birr by September. Diesel and kerosene followed a similar path, reaching just under 80 birr per litre by late 2023.

This phase allowed businesses some room to adapt. Transporters revised tariffs gradually, importers adjusted pricing assumptions, and contractors absorbed higher costs into longer project timelines. By July 2024, gasoline had reached about 83 birr per litre, with diesel and kerosene close behind at 84 birr.

The turning point came in late 2024. A sharp rise in October 2024, which pushed gasoline above 91 birr per litre, was followed by a rapid succession of adjustments in January, March and May 2025. Within five months, gasoline climbed from 101 birr to 123 birr per litre, while diesel rose from 99 birr to 116 birr. The final adjustment in December 2025, which unified prices at 129 birr, cemented a new, higher plateau.

Transport as the inflation engine

Fuel matters everywhere, but in Ethiopia it matters more than most. Diesel is the backbone of long-haul logistics, powering trucks that move imports from Djibouti, cement from factories, agricultural produce to markets and construction materials to sites. It also runs generators that compensate for grid interruptions across industry and commerce.

Each fuel adjustment therefore transmits quickly into prices across the economy. Freight costs rise first, followed by wholesale prices, then retail. In construction, higher diesel prices inflate the cost of cement, steel and aggregates even before labour and financing are considered. In food markets, transport costs compound supply shocks, magnifying volatility.

Economists note that fuel-driven inflation is particularly difficult to contain because it affects both the cost of production and the cost of distribution. When diesel prices rise by double digits, the effect ripples far beyond petrol stations.

FX exposure and the import bill

Unlike oil-producing economies, Ethiopia imports all refined petroleum products. Domestic pump prices therefore reflect a complex interaction of global oil prices, shipping costs, exchange rates and the availability of foreign currency.

As the birr has faced sustained pressure, fuel pricing has increasingly acted as a release valve, passing external costs through to domestic consumers and businesses. For the government, this reduces the fiscal burden of subsidies and preserves scarce foreign exchange. For companies, it introduces a layer of uncertainty that is difficult to hedge.

The impact is uneven. Large logistics operators with diversified fleets and pricing power can adjust more quickly. Smaller transporters, where fuel can account for 30–40 per cent of operating costs, face acute margin pressure. Fixed-price contracts become loss-making almost overnight, eroding working capital and accelerating wear on ageing fleets.

A new operating environment

The lesson of the past three years is not merely that fuel prices have risen, but that the pattern of adjustment has changed. Long periods of stability can no longer be assumed. Instead, businesses must plan for step increases that arrive with limited notice and substantial magnitude.

This has begun to reshape corporate behaviour. Fuel escalation clauses are becoming more common in logistics and construction contracts. Quotation validity periods are shortening. Route optimisation, load efficiency and fleet renewal have moved from operational concerns to strategic priorities.

Where alternatives exist, companies are beginning to explore them more seriously. Electrification for short-haul delivery, LNG for heavy trucks, and more efficient diesel engines are no longer experimental concepts but cost-containment tools.

The policy signal

From a policy perspective, the fuel price staircase sends a clear message. Ethiopia is moving steadily away from price shielding toward a system that reflects import costs more transparently. While this improves fiscal sustainability and foreign exchange management, it shifts adjustment costs onto the private sector and households.

In the short term, this raises inflationary pressure and complicates business planning. In the longer term, it may encourage efficiency, energy substitution and investment in alternative transport technologies. The transition, however, is unlikely to be smooth.

Looking ahead

With fuel prices now more than double their early-2023 levels, the question for businesses is less about whether prices will rise again, and more about how often and how sharply. Volatility, rather than absolute price levels, has become the defining risk.

For Ethiopia’s economy, fuel will remain a powerful transmission channel for global shocks and domestic policy choices alike. How effectively businesses adapt to this reality will shape competitiveness, investment decisions and inflation dynamics well into the second half of the decade.

Prices are official pump prices reported by authorities and business news sources; regional variations may apply.