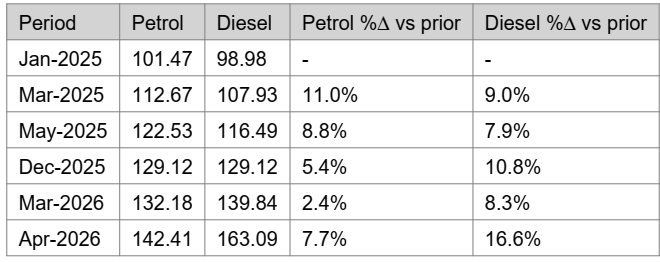

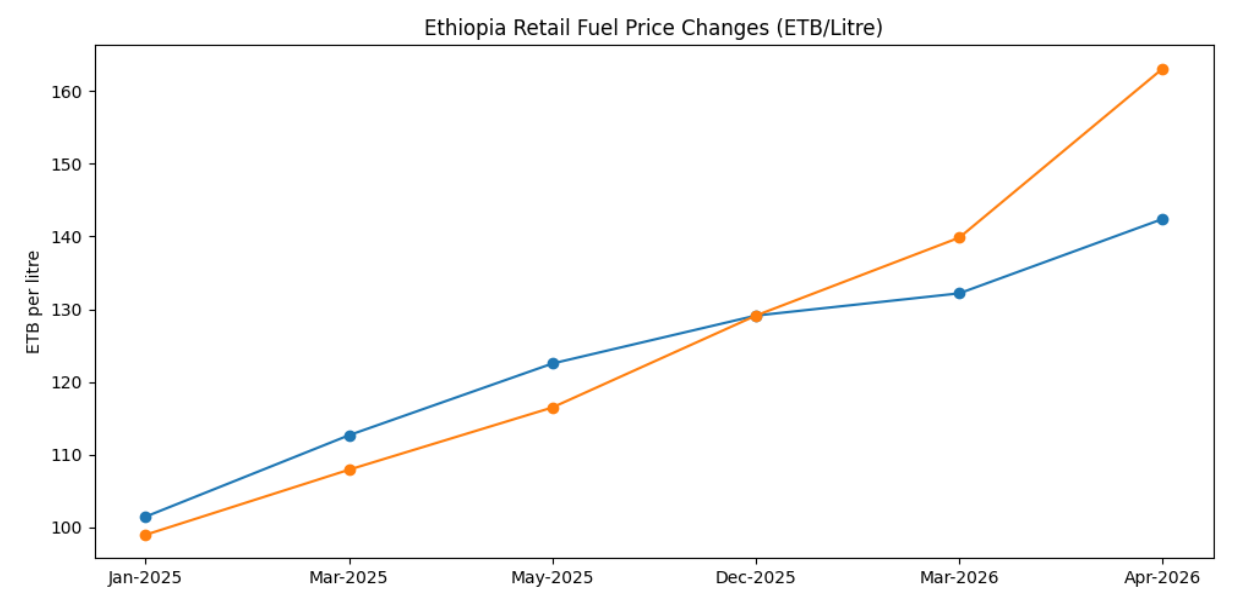

Ethiopia’s fuel story is becoming less about phased domestic price liberalisation and more about external vulnerability. Recent pump-price adjustments have pushed petrol and diesel prices materially higher than levels captured in the earlier “fuel staircase” analysis, reinforcing how domestic pricing now transmits international shocks faster into the local economy. What had been a controlled subsidy-withdrawal story is increasingly evolving into a supply-security and imported inflation story.

The bigger shift is geopolitical.

Tensions around the Strait of Hormuz—through which roughly a fifth of global seaborne oil flows—have exposed how quickly maritime disruptions can raise risk premiums, freight costs and supply anxieties, even when outright physical shortages do not materialise. For a fuel-import dependent economy like Ethiopia, that exposure matters beyond the forecourt. Higher diesel prices feed directly into trucking rates, dry-port charges and inland logistics costs. That raises pressure on imported consumer goods, construction inputs, agricultural distribution and export competitiveness. In effect, energy volatility increasingly acts as a transmission mechanism for broader cost inflation.

The concern for policymakers is not simply whether global oil prices spike, but whether repeated disruptions make import financing more expensive. If freight insurers, traders or suppliers begin pricing in persistent geopolitical risk, Ethiopia’s fuel bill could rise even without a sustained surge in crude benchmarks.

There is also a foreign exchange dimension. Higher fuel import costs place additional pressure on hard-currency demand at a time when businesses already face elevated funding costs. For an economy managing both import dependence and FX constraints, this can compound macroeconomic stress. Temporary easing in global crude prices following signals of reduced disruption offers some relief, but it does not remove the structural risk. The market’s message is that supply routes matter as much as oil prices.

That changes the policy conversation.

The strategic question is shifting from how Ethiopia manages pump-price adjustments to how it strengthens resilience against external energy shocks—through supply planning, import financing flexibility and logistics risk management. In that sense, the real risk may no longer be the next price increase itself, but the fragility that repeated external shocks could expose.